When Should You Claim Social Security Benefits

Yep, we’re engulfed in tax season, but we thought you might like some guidance in an arena where we’ve noted an uptick of inquiries to us during our tax planning or preparation sessions. It’s now becoming clear to us and other financial planning colleagues that recent economic conditions and legislative changes warrant a reassessment of both Social Security claiming strategies and retirement‑phase tax planning. While conventional guidance has often emphasized delaying benefits to age 70, the economic value of that strategy has narrowed. At the same time, new age‑based deductions for seniors introduce additional—but often misunderstood—tax planning considerations.

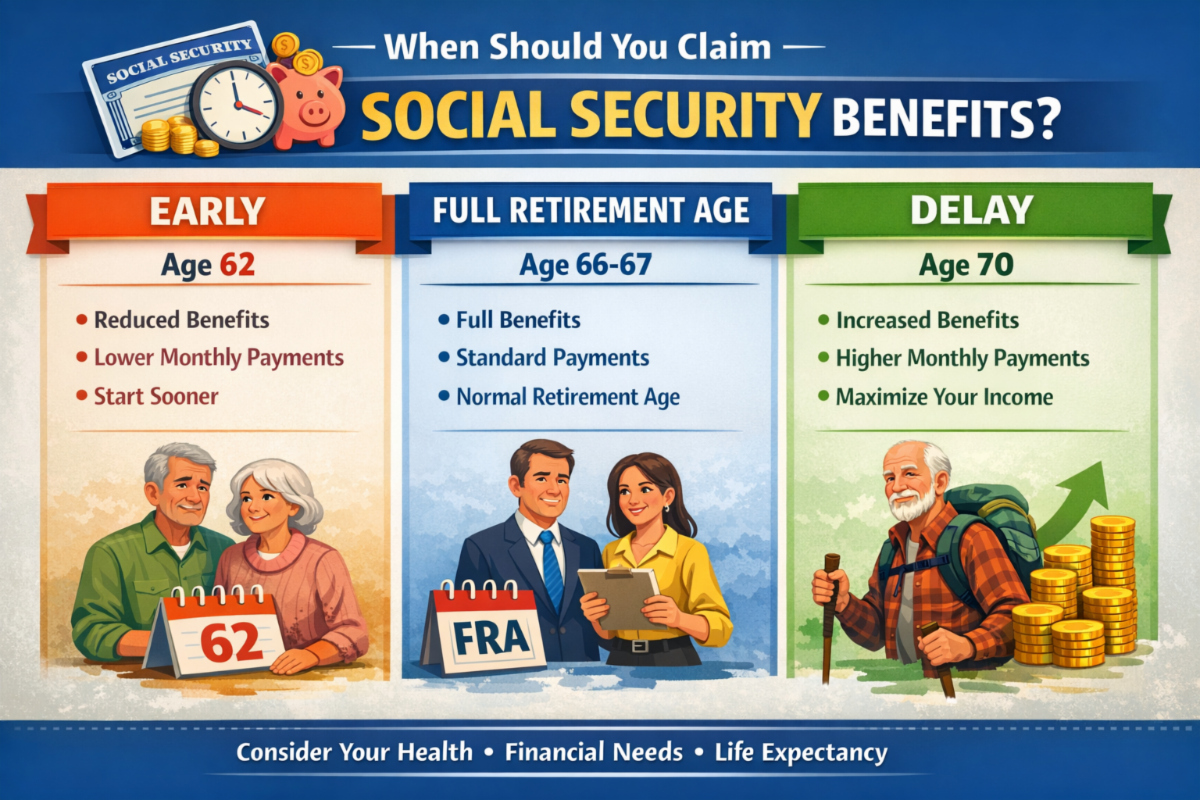

Re‑Evaluating the Economic Case for Delaying Social Security

Under current law, Social Security retirement benefits increase by approximately 8% per year for each year benefits are deferred beyond full retirement age (FRA) up to age 70, exclusive of cost‑of‑living adjustments. Historically, this deferral strategy appeared compelling when interest rates were so low, often near zero.

However, higher prevailing interest rates materially reduce the present‑value advantage of delayed claiming. Discounting future benefit streams at today’s higher real rates often results in expected gains in the low single‑digit range—commonly estimated at approximately 1%–5% for a typical married couple at age 67, depending on mortality assumptions and discount rates. Truth be told that while we at Abo and Company often address such inquiries conceptually, we’ve found many of our financial planning colleagues and investment advisors better equipped and less expensive than us to run such figures with their customized software.

Planning implications

- For married couples, optimal claiming frequently involves delaying the higher earner’s benefit (to maximize survivor benefits) while permitting the lower earner to claim earlier.

- For single individuals in good health, delaying may still function as longevity insurance, particularly where other income sources are sufficient to fund early retirement years.

- For households with liquidity constraints, shorter life expectancy assumptions, or higher opportunity costs, earlier claiming may be economically rational.

The key takeaway is that delaying to age 70 is no longer just an automatic optimal strategy and should be evaluated in conjunction with portfolio return assumptions, mortality projections, and tax considerations. Still, we encourage financial planning colleagues and investment advisors to our clients at least keep us in the loop with regard to their analysis and suggestions. If you need the name or names of seasoned financial planners (and ones that return phone calls), feel free to ask us at Abo and Company.

New Senior Deduction

Beginning in tax year 2025, taxpayers age 65 or older may claim a new temporary $6,000 above‑the‑line deduction, enacted under recent legislation and often colloquially referred to as “No Tax on Social Security”.

- The deduction is per qualifying taxpayer, not per return.

- Married couples where both spouses are age 65 or older may claim up to $12,000.

- The deduction is available regardless of whether the taxpayer itemizes or claims the standard deduction.

Critically, there is an important distinction between a “deduction” and an “exclusion”. This provision does not exclude Social Security benefits from gross income. Instead, it functions as an additional deduction that reduces taxable income, not provisional income.

As a result:

- The statutory formula determining whether Social Security benefits are taxable remains unchanged.

- Taxpayers whose benefits were previously partially or fully taxable may continue to face benefit taxation.

- The deduction may reduce marginal tax liability, but it does not alter the inclusion thresholds that govern Social Security taxation.

This distinction is particularly important for clients who might have been led to believe and even expected a wholesale elimination of taxes on Social Security benefits.

Age‑Based Eligibility Creates Planning Nuance

Another source of confusion is that eligibility is age‑based, not benefit‑based:

- Taxpayers over 65 qualify even if they have not yet claimed Social Security.

- Taxpayers under age 65 do not qualify, even if they are already receiving Social Security benefits.

From a planning perspective, this creates timing considerations around retirement, benefit claiming, and income recognition that may influence Roth conversion strategies, capital gain realization, and withdrawal sequencing.

Abo and Company Planning Takeaways

- The economic benefit of delaying Social Security should be reassessed using updated discount rates and mortality assumptions.

- Claiming strategies should be coordinated with survivor planning, portfolio withdrawals, and tax‑bracket management.

- The new senior deduction may lower overall tax liability but does not eliminate Social Security taxation.

- Misunderstanding the distinction between deductions and exclusions could lead to incorrect tax projections.

Given the interaction between benefit claiming, tax thresholds, and income timing, integrated retirement and tax modeling is more important than ever.

Abo and Company, LLC

Abo Cipolla Financial Forensics, LLC

Certified Public Accountants / Litigation & Forensic Consultants

307 Fellowship Road, Suite 202, Mt. Laurel, NJ 08054

Phone: 856-222-4723 Fax: 856-222-4760

---------------------------------------------------------------------------------------------------------------------------------------

This submission is provided by Abo and Company, LLC, Certified Public Accountants, for their clients, advisors and other interested persons. Since technical information is presented in a generalized fashion, the communication is not meant to replace the need for competent professional advice and the reader should understand that the information contained in or made available through this communication is not intended to be a substitute for the services of trained professionals in any field. As such, the reader should evaluate and bear all risks associated with the use of any comments, including any reliance on the accuracy, completeness, or usefulness of such content.

Any tax advice that may be contained in this communication, (including attachments) is not intended or written to be used, nor can be used, by any recipient of this communication for the purpose of (i)avoiding penalties that might be imposed pursuant to the Internal Revenue Code or U.S. Treasury Regulations, or applicable state or local law or regulation or (ii) promoting, marketing or recommending to another party any tax-related matters addressed herein.